I would like to share with you on my thoughts on the lastest purchase of Google by Berkshire Hathaway.

Warren Buffett’s Biggest New Bet: Alphabet (Google)

By Charlie Tian

Berkshire Hathaway’s latest 13F filing, released Friday, shows the firm’s largest new position of the quarter: a $4 billion stake in Alphabet (GOOGL). Although Berkshire has traditionally been wary of major tech investments—and Buffett and Munger have openly acknowledged missing the chance to buy Google years ago—this sizable purchase likely reflects Buffett’s own decision rather than that of his investment managers, Todd Combs or Ted Weschler.

Why Alphabet Fits the Buffett Playbook

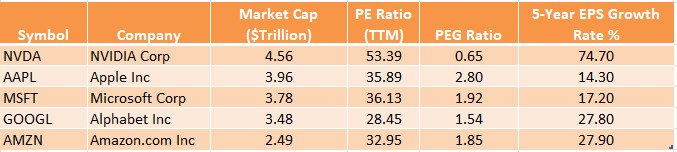

Among the market’s top five largest companies, Google currently carries the lowest price-to-earnings ratio. Its Price-to-Earnings-to-Growth(PEG) ratio trails only Nvidia’s—but Nvidia’s growth rate is significantly higher, explaining the difference. Below are the market caps, valuations, and growth rates of these leading companies.

Date: Nov. 17, 2025. Source: GuruFocus.com.

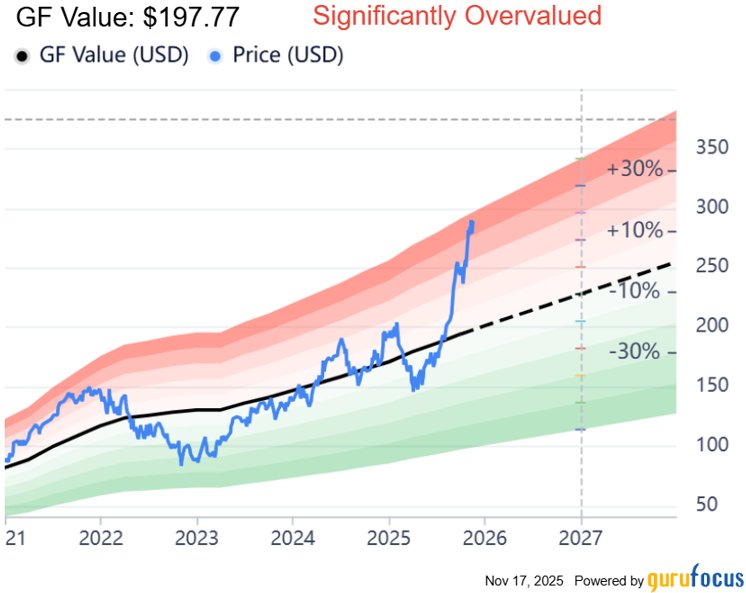

In our previous article, we highlighted the GF Value metric as a superior tool for assessing valuation. Looking at Alphabet’s current GF Value, the stock now seems overvalued. However, Berkshire made its purchase during the third quarter - when, according to the GF Value chart, Alphabet was trading at a fair valuation in July and August. This once again underscores why the GF Value framework provides a more reliable gauge of intrinsic value.

Date: Nov. 17, 2025. Source: GuruFocus.com.

Warren Buffett has always emphasized buying great businesses at fair prices, and today Alphabet fits that philosophy exceptionally well. It’s true that Buffett missed Google during its early hyper-growth years—just as he initially did with Apple. But consider this: since Berkshire began accumulating Apple shares in 2016, the stock has increased more than tenfold. With that precedent in mind, it’s easy to see why Berkshire might now be taking a closer look at Google’s quality and valuation.

1. A wide and durable economic moat

Google Search continues to dominate the global information-discovery landscape. Its massive scale, unparalleled data advantage, and deeply ingrained user habits form the type of long-lasting competitive moat Buffett has always prized.

2. Strong, consistent profitability

Alphabet’s advertising machine generates enormous free cash flow—recurring, resilient, and remarkably stable across economic cycles. That level of predictability aligns perfectly with Berkshire’s preference for dependable compounders.

3. A reasonable valuation for a tech leader

Among mega-cap technology companies, Alphabet trades at one of the most modest earnings multiples. For Berkshire, that likely makes it a classic “growth at a fair price” opportunity rather than a speculative high-valuation bet.

4. A long runway in AI and cloud

Alphabet sits at the center of several secular growth trends—AI, cloud infrastructure, and YouTube monetization. These are long-term tailwinds that strengthen the company’s already robust core business.

Quality, Growth and Valuation

Warren Buffett may be retired, but the Buffett effect is alive and well. Google shares jumped more than 3% today, even as the broader market traded down almost 1%.

For investors, it’s a reminder that Alphabet offers a rare combination: a dominant competitive moat, steady and reliable profitability, and meaningful exposure to the future of AI. While the stock now trades above the levels where Berkshire likely bought in, its valuation remains relatively reasonable compared with other members of the trillion-dollar club.

About: Charlie Tian, Ph.D. is the founder and Chief Executive Officer and portfolio manager of GuruFocus Investments, LLC, an SEC-registered investment management firm.

Read More Blogs:

- Visa and Mastercard in an AI World: Separating Fear from Reality

- Overvalued Market, Uneven Returns: Where to Look Next in 2026

- 3 Undervalued Wide-Moat Stocks You May Be Overlooking

- Berkshire's Biggest New Bet: Alphabet (Google)

- GuruFocus (GF) Value: a Better Valuation Measure vs. PE

This research report has been prepared by GuruFocus Investments, LLC, an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Registration as an investment adviser with the SEC does not imply a certain level of skill or training.

The information contained in this report is provided for informational and educational purposes only and should not be construed as investment advice, an offer, or a solicitation to buy or sell any security or to participate in any investment strategy. Any opinions or views expressed herein are those of the author(s) and are subject to change without notice.

GuruFocus Investments, LLC does not accept liability for the content of this email, or for the consequences of any actions or inactions taken on the basis of the information provided. The content of this email is not investment advice and any opinions or assertion contained in this email do not represent the opinions or beliefs of GuruFocus Investments, LLC or any of its respective employees.

The information presented is believed to be reliable, but its accuracy and completeness cannot be guaranteed. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal.

This communication is intended solely for the use of the individual or entity to whom it is addressed. Unauthorized use, distribution, or copying of this communication or its contents is prohibited.